- Home

- About Us

- Services

- HR Guide

- Jobs

- Education

- Contact Us

Provident Fund (PF) is a government-regulated retirement savings scheme in which both the employee and employer contribute monthly to build a secure financial corpus for the future.

A Provident Fund (PF) helps employees accumulate a secure financial corpus for retirement. Regular contributions from both employer and employee ensure a lump sum retirement fund, providing long-term financial stability.

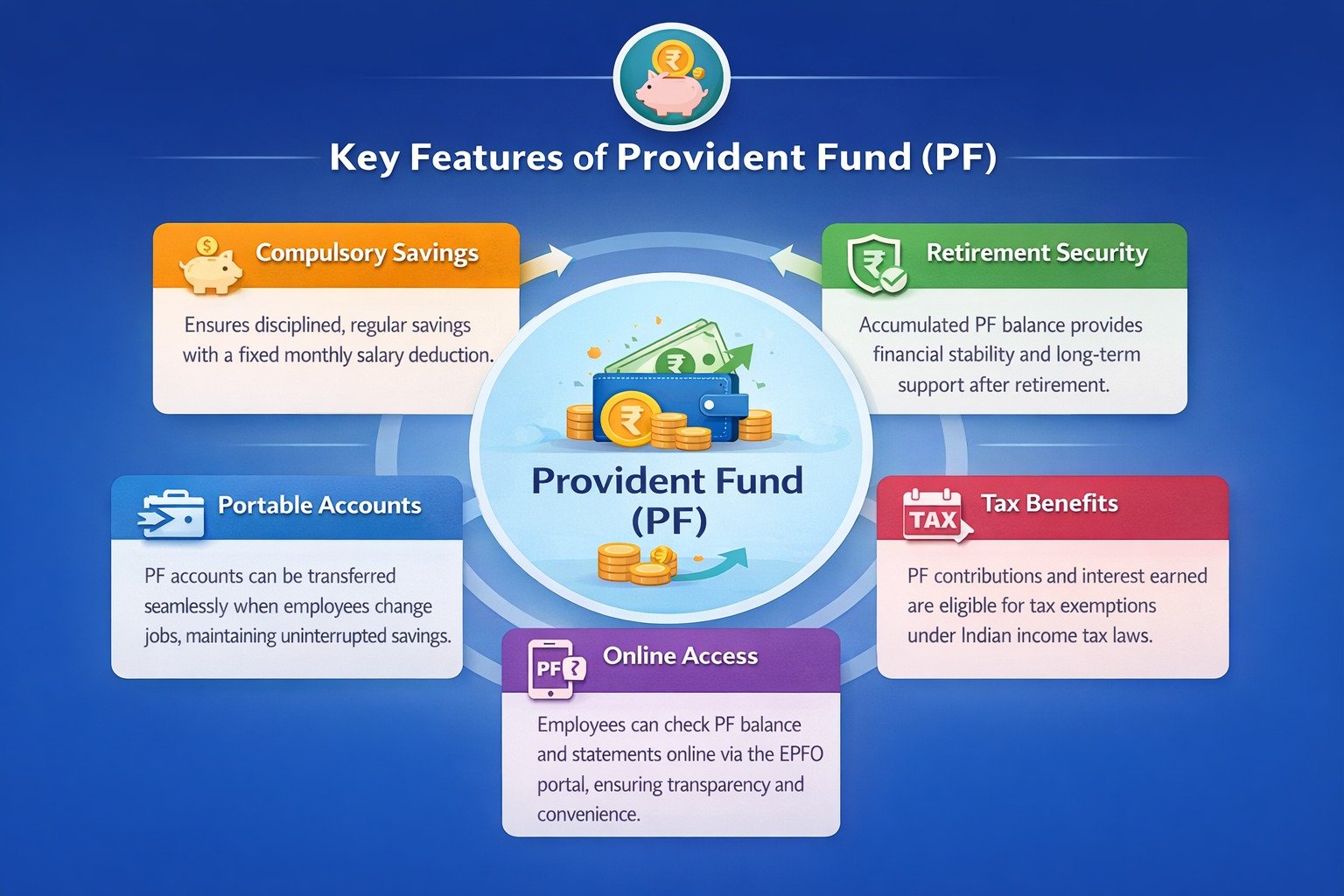

PF promotes a consistent savings habit, as a fixed portion of salary is automatically deposited every month, helping employees save effortlessly for the future.

PF balances earn government-declared interest rates, making it a safe, reliable, and steady investment option with predictable returns.

Contributions and interest earned in a PF account are eligible for tax exemptions under Indian income tax laws, helping employees reduce their tax liability legally.

Partial PF withdrawals are allowed for medical treatment, education, marriage, housing, or other emergencies, providing quick financial support when needed.

PF accounts are fully portable, allowing employees to transfer their PF balance when switching jobs, ensuring uninterrupted savings and benefits.

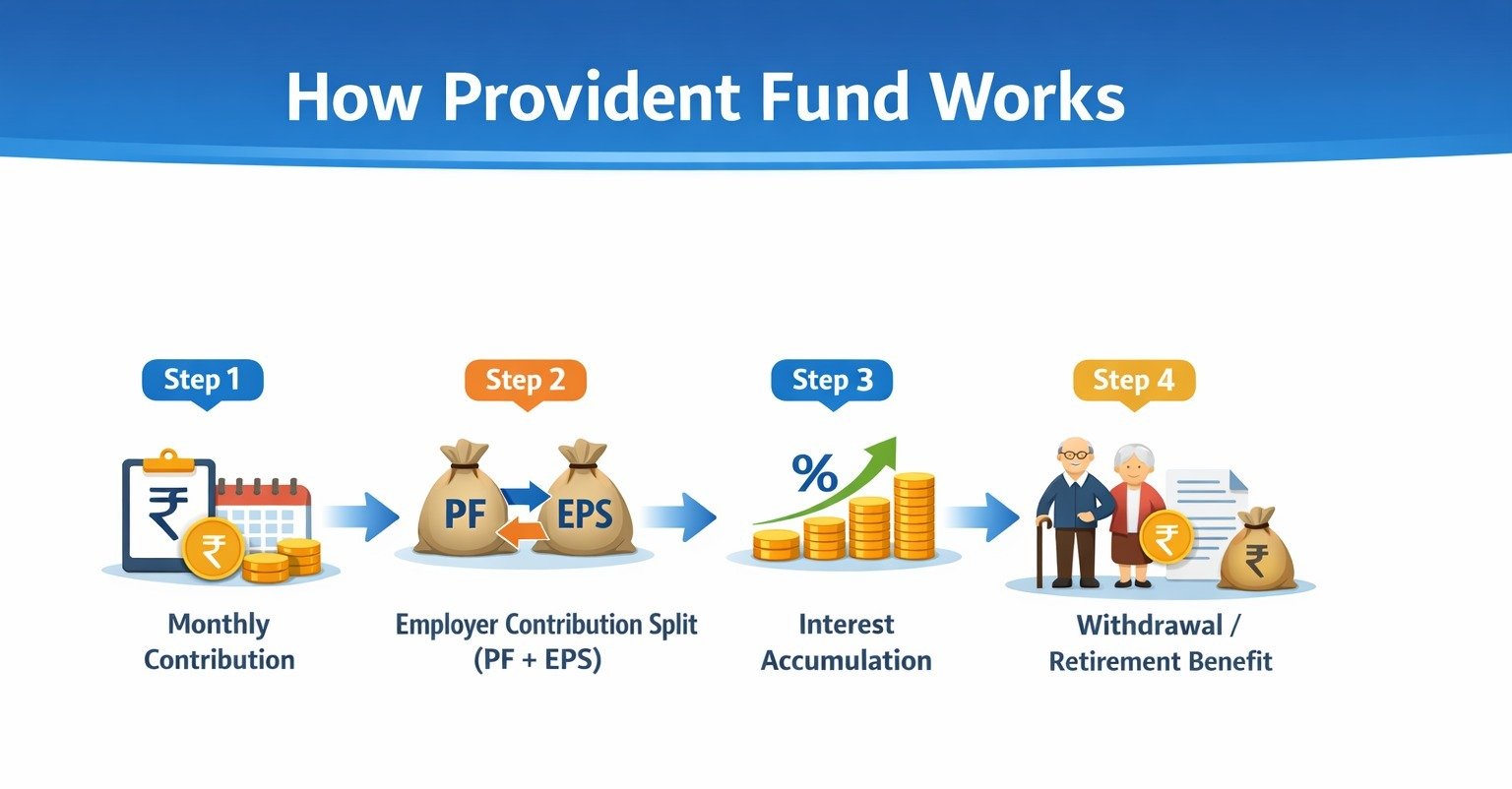

A fixed percentage (typically 12% of Basic Salary + DA) is deducted from the employee’s salary and deposited into their PF account. Employers contribute an equal or specified percentage, including 3.67% to PF and 8.33% to Employee Pension Scheme (EPS), ensuring a combined savings pool for retirement benefits.

The total PF balance, including employee and employer contributions, earns government-declared interest rates, providing a secure and steadily growing retirement fund over time.

Employees can make partial withdrawals for emergencies such as medical treatment, education, marriage, or housing. The full accumulated balance, including contributions and interest, can be withdrawn upon retirement or after completing the specified service period, ensuring long-term financial stability.

PF contributions and interest earned are eligible for tax exemptions under Indian income tax laws, making it a tax-efficient retirement savings option for employees.

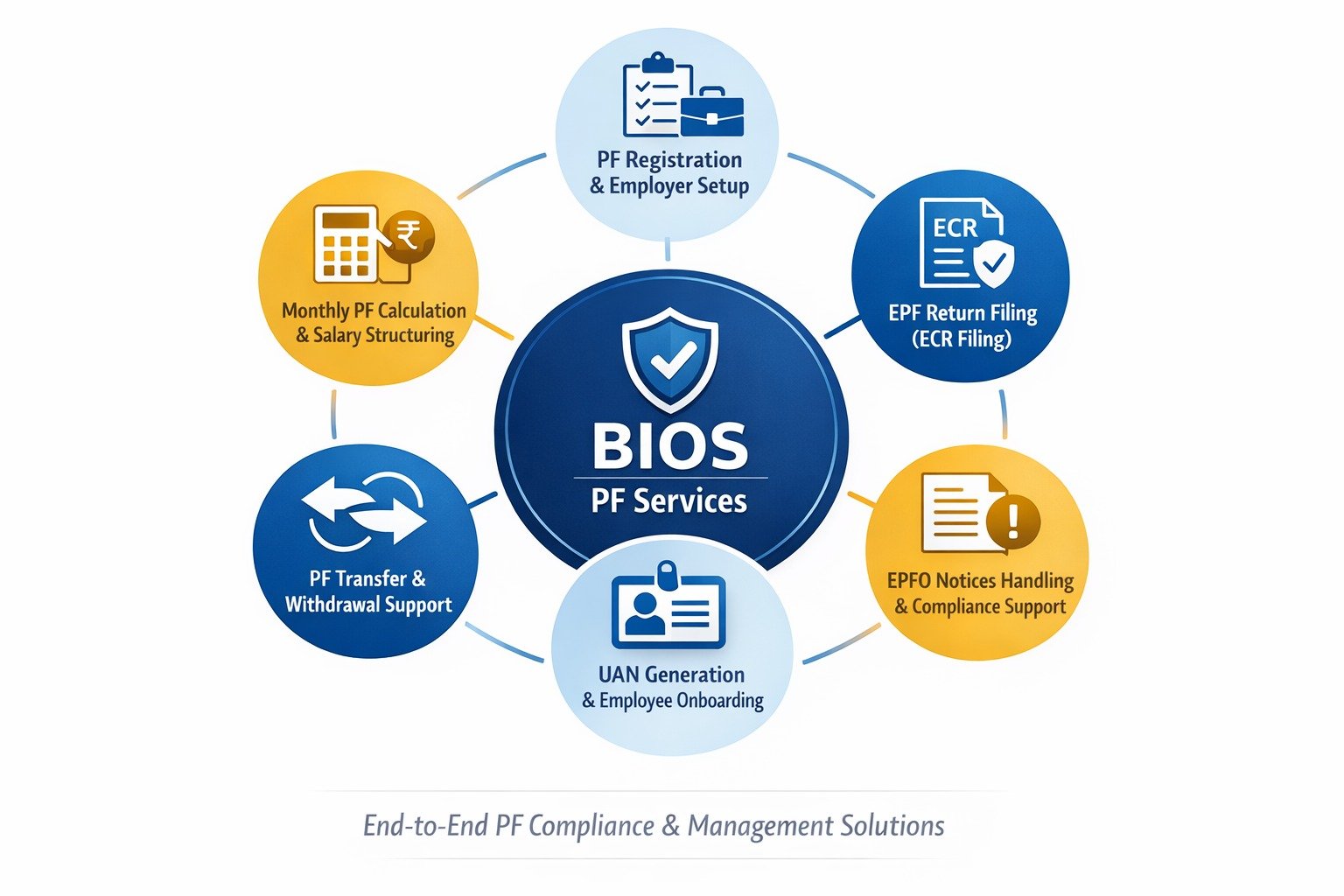

Ensure 100% accurate PF management with BIOS experts. Avoid penalties & stay compliant effortlessly.

BIOS intends to be an organisation offering world class Quality, Reliable and Transparent service by being transcendent and to spread its wings and to soar to great heights.

© Copyright 2026 BIOS India

Designed by ![]()

First Floor, Ranjesha Building Kochapilly Appachan Lane, Opp POC Near NH Bypass Palarivattom Jn. Alinchuvadu, Edapally PO Ernakulam. Kerala

First Floor, Ranjesha Building Kochapilly Appachan Lane, Opp POC Near NH Bypass Palarivattom Jn. Alinchuvadu, Edapally PO Ernakulam. Kerala Staffing Solutions

Staffing Solutions Management Consulting

Management Consulting